Random thoughts that attempt to shed light into the world of venture capital and entrepreneurship from Chip Hazard, General Partner at Flybridge Capital Partners.

Almost eight years ago, Dr. Emre Gençer, a principal research scientist at MIT, and some of his colleagues saw a challenge in the Industrial sector and its drive to decarbonize. On one hand, the Industrial sector accounts for 34% of global greenhouse gas emissions, so the need for innovative solutions was clear. On the other hand, for leaders of these companies, making decisions is hard given evolving technologies, a myriad of potential tradeoffs, capital intensity, and a high degree of complex interrelationships across the industrial sector. Emre feared that without an effective way to model and optimize decisions, Industrial companies would either invest in less-than-ideal ways or, more likely, defer essential decisions that could have a significant positive impact on their carbon footprint and operating costs.

This insight led to the creation of Sesame, an innovative software suite that simulates and optimizes the costs and emissions associated with decarbonization investments in heavy industry. Sesame is backed by seven years of deep research at MIT to develop both the data and the models to handle the complexity of these simulations, the tradeoffs and interrelationships therein, and the ongoing operating decisions and investments that will result. Working from plant-level data on up, the system offers economic, environmental, and systems analysis capabilities to accurately and rapidly evaluate industrial decarbonization solutions at scale and in so doing, they become a single source of truth from which optimal decisions can be made.

When we first met Emre and his co-founders Paul and Jim (shown below in the obligatory first-day founder selfie) last year, we were immediately drawn to the depth of their insights, the completeness of the solution that had created at MIT, the strong customer backing, their compelling plan to commercialize the platform in a software sector that analysts expect to exceed $9B by 2030, but most of all their passion for the space and the mission to drive effective decarbonization decisions across the heavy industry segment.

One of my greatest joys as a VC – and one that correlates with success – is the opportunity to work with deeply talented, exceptional founders looking to turn their passions and life’s work into a company that can succeed and thrive in the market. As a result, we immediately committed to work with the team to spin Sesame out of MIT, provide the initial financing, and partner with the team to build a compelling company over the coming years. Our friends at Powerhouse Ventures join us in this commitment and we are excited to see the company launch this week. More on this exciting company can be found in its announcement, website, and this excellent post from the Powerhouse Ventures team.

For enterprises to be able to achieve the vision of our AI-powered future, they need to deploy applications and the underlying models confidently. Not only confident of the underlying performance and accuracy but also from a security perspective. Customers need to know the models will not inadvertently reveal PII or other sensitive information, that end users will not be able to prompt the models into toxic behavior, and that their models are safe from various current and emerging threat vectors from malicious actors. Further, they need to deploy these security solutions in a way that fits seamlessly into their existing IT infrastructure without compromising performance and reliability.

For the last few years, TrojAI founders James Stewart and Stephen Goddard have developed the leading enterprise AI security solutions to instill that confidence in their customers. Earlier today, the company announced that Flybridge and Flying Fish Ventures co-lead a financing, alongside Alteryx Ventures, to drive the company’s growth forward.

In our diligence on the investment opportunity, we heard customer success stories firsthand, including from a Fortune 50 financial services company where TrojAI protects hundreds of models and safeguards the AI usage of tens of thousands of employees. All in production, at scale, and without compromising performance. This validation not only caught our attention but is also one of the reasons that CB Insights named the company to the AI 100 list of the most promising artificial intelligence startups of 2024. A proven market-leading product targeting a critically important and large market opportunity was the first pillar of our investment thesis.

The second pillar of our investment thesis was that Lee Weiner joined the company as CEO as part of this financing. Lee is an accomplished leader in the cybersecurity market who has repeatedly delivered innovative solutions to enterprise customers. Most notably, for the last 11 years, Lee was a senior executive at Rapid7, leading products, engineering, and innovation as the company scaled from $40 million to over $750 million in revenue. As one of our friends at Rapid7 told us, Lee simply knows how to deliver for customers and is an exceptional leader.

We are thrilled to invest in the success the Founders of TrojAI have created and to see Lee and the entire team applying their expertise to the company’s continued growth and success.

I used to own a Chevy Bolt. Sparky was its name, and it was a high-quality commuter car. One day, a couple of years into ownership, a battery defect caused Bolts to catch fire unexpectedly, and my office garage put up a sign saying that Bolts were no longer allowed in the building. Sparky, now garageless, was very sad.

Electrification has the significant potential to mitigate emissions and decarbonize energy supply chains, making it an important strategy for reaching net zero goals. However, doing so requires high-quality, affordable, and powerful batteries. As my Bolt story shows, for any complex engineered product to reach mainstream production levels and adoption, a robust quality control system is required. Sadly, Sparky will not drive the electrification revolution.

The same was true for the Semiconductor market, where companies like KLA (nearly $10B in revenue and a $100B market cap) enabled the industry to increase yields and improve quality with a suite of monitoring, inspection, and review tools that are now used throughout the chip fabrication process.

As a result, and in addition to the company fitting squarely within our AI-infused complex systems thesis, when Jeff Peters of Ibex Mobility introduced us to the team from Glimpse, we were immediately attracted to the investment opportunity. The three founders – Peter Attia, Patrick Herring, and Eric Moch have a combined 25 years in the Li-ion battery industry, including deep industry (Tesla and Toyota) and academic (Stanford and Harvard PhDs) expertise.

(Left to right: Patrick, Peter, and Eric)

Through this first-hand experience, they realized that the lack of adequate battery quality inspection technology was holding back the industry and our electrified future; preventing the ramp-up of Gigafactories; costing the industry billions in the form of lower yields and field-found defects; and leaving Sparky and I in the dust (of on-street parking).

The Glimpse team leveraged their domain understanding to design from the ground up a high-throughput, high-accuracy, battery quality inspection platform optimized for high-volume battery production and battery assembly environments. The company’s platform marries CT scanners, which they saw the power of in a lab setting at Tesla, with a modern AI-powered analytical software stack and data pipeline to drive unprecedented customer results.

We closed a seed round alongside Ibex Mobility in 2023, and today (ahead of schedule), the company is launching with paying customers in production. If you are intrigued as to what the future of battery quality inspection looks like at scale, they also released into the public domain a dataset of 1,000 batteries that were scanned and processed by the Glimpse technology, which can be found in their portal here.

We are thrilled to back this talented team, tackling a hard and important problem that will help drive a safe and rapid transition to an electrified future and make Sparky (RIP) happy again.

Over our 22-year history, Flybridge has always focused on investing in trends that will define business and society in the future. In fact, our name is a nod to the highest deck on a boat, offering an unobstructed view of the waters ahead. From this vantage point, we scout for opportunities and look for ways to partner with Founders who are pioneering and shaping the future.

The future we see today is a world permeated by Artificial Intelligence. There will be no such thing as an AI company, as every company will be an AI company. Our focus as a firm is solely to back ambitious Founders at the pre-seed and seed stages who are creating and building transformative companies for this AI-powered future.

Source: DALL-E, “A Future Woven with Intelligence”

We are not new to this space. Our first wave of AI and ML investments were in companies focused on using data to derive insights, allowing companies to improve decision-making. We told graduates to “Forget Plastics – it’s all about Machine Learning” in 2012, and we christened this cohort of companies as Full-Stack Analytics companies in 2014. Portfolio companies from this time include a 2010 seed investment in ZestAI, a pioneer in leveraging AI for Underwriting, and a 2011 pre-seed that we led in BitSight, an ML and data-powered pioneer in the Cybersecurity Risk Management market.

Our second wave of AI investments fell into the category of what we termed in 2019 as Applied AI companies. We noted that the application layer of AI ultimately drives the business value, but effectively doing so requires a deep understanding of the domain, the specific workflows that AI will seek to improve and optimize, and how best to incorporate AI into end-user experiences to engender trust and drive engagement. Portfolio companies operating within this thesis include Aiera, Bowery, Brighthire, Proscia, and Syrup.

Throughout both waves, we leveraged our long history of investing in infrastructure to back Founders building platforms to (1) manage and operationalize data and (2) make it easier for developers to build, deploy, and manage high-performance mission-critical applications. These investments include companies such as MongoDB, which we first backed in 2009 and which today is a leading company in the “AI Stack” with over $1.6B in annual recurring revenue, as well as other developer experience and “modern data stack” companies such as Firebase, FeatureLabs, Datalogue, and Stackdriver.

In the last 18 months, the capabilities of AI systems have taken a massive leap forward. A combination of technical advances drove this leap — the marriage of globally connected infrastructure, which created massive data sets upon which AI systems could train, exponential increases in computing power per dollar, and wildly sophisticated software techniques. These core foundations are joined with an unprecedented level of technical understanding, speed of advancement, and adoption by enterprises, developers, and consumers.

The future potential this creates exhilarates us, and, as a result, we no longer view AI as one of our investment sectors but rather our sole focus — the nucleus of the next industrial transformation.

Flybridge’s Investment Focus: Five Insights into the Future

We are looking to partner with ambitious founders building along one of five dimensions. While we believe every company will eventually become an AI company, in today’s world, an AI-powered company means more than just using AI as a supplementary tool. It implies that AI is a core element of the company’s value proposition and provides unique customer value. This integration means that AI is deeply embedded in the company’s primary product or service, significantly influencing its strategy and operational processes.

1. Vertical SaaS that is AI native

By building and providing fully integrated solutions that are purpose-built for vertical-specific industries, a new generation of SaaS companies that are AI native have an opportunity to carve out massive market opportunities, building on top of the rapidly evolving horizontal tools offered by big tech, emerging AI platforms for builders and operators, and the open source community. As more traditional software capabilities commoditize (driven in large part by AI-powered co-pilots making it easier to develop applications), enduring and successful Vertical SaaS companies will not only streamline workflows but also will generate the outputs and insights these systems previously enabled humans to perform. As a result, we believe that over $1 trillion in vertical SaaS revenue is “up for grabs” in the coming decade and are excited to back Founders participating in this transformation. Some AI native Vertical SaaS companies in the extended Flybridge portfolio include Aiera, DayZero, Entr, Finkargo, Forcemetrics, H2Ok Innovations, Hansa, noetica, Porosity, Proscia, and Syrup.

Successful Founders in this market will need to deeply understand customer requirements, build quickly, develop self-reinforcing data moats, and create unique value for their customers through well-designed user experiences that build trust, drive usage, and create new experiences that make individual contributors and teams far more efficient and effective. Our colleagues Julia and Daniel expanded on this here and here.

2. Horizontal Applications that are AI native

Artificial Intelligence promises to improve decision-making, streamline operations, and generate outputs and insights, but realizing this promise requires building these capabilities into an application. By providing functional capabilities that bring AI practices to horizontal workflows that cut across industries, Founders can help companies realize the AI vision of operational efficiencies while tapping massive TAMs that disrupt existing non-AI-native incumbents. We believe the discontinuous innovation that AI can introduce into the Horizontal SaaS market — expanding the market dramatically through increased automation — puts over $3 trillion in revenue “up for grabs” over the next ten years. Some companies building AI-native horizontal applications in the extended Flybridge portfolio include Brighthire, MelodyArc, Meritic, Quilt, Tato, and Teal.

3. Data infrastructure and platforms for AI application builders and operators

As a team, we have seen significant success supporting Founders who are building developer data platforms. These companies have typically seized upon massive technical shifts, for example, the rise of the cloud, to create platforms purpose-built for the new architectures, use cases, and deployment patterns. AI represents another such shift, and Founders creating solutions to make applications easier to build, run, manage, secure, and monitor will thrive. Not only will new applications emerge, but also the underlying models – especially if fine-tuned and open-source – and model infrastructure (vectors, knowledge graphs, etc) create a new part of the stack to be developed and managed. Further, as we know, AI models are only as good as their training data and how models apply inferences to data in a timely manner. As a result, for many customers, the AI journey begins at the data layer, and we believe companies building the “modern data stack” will see the same success in the coming AI application boom as those companies that make it easier to build, deploy, run, and manage these applications. Taken together, we believe these markets will exceed $200 billion in annual revenue within ten years. In addition to prior investments in companies such as MongoDB and Firebase, some of the companies building data infrastructure and platforms for AI application builders and operators in the extended Flybridge portfolio include Appwrite, Arcee, Avala, Blaze, FiveOneFour, 5x, Flojoy, Freeplay, Metaplane, Portkey, and Xata.

These first three areas will come to dominate the enterprise software market, disrupting incumbents who will race to keep pace with new capabilities and trends. Outside the traditional enterprise technology realm, we are excited about — and have actively been investing in companies — in two additional emerging areas.

4. AI infused complex systems

In our Applied AI position paper published in early 2019 (here), we observed that in some cases, the best way to capture the value an AI-based system creates would be through selling a complete product or vertically integrated system. Each industry has different dynamics in this regard, but one example of the systems approach is Tesla selling autonomous EV automobiles versus providing autopilot or battery control systems to other OEMs. Given the dynamics of the auto industry and consumer preferences, a company could capture more value with a complete system (Tesla has a $780B market cap) versus being a vendor to the industry (Cruise was a billion-dollar acquisition). However, full systems companies in fields such as robotics have historically been challenging for seed-stage investors. They are complex — requiring multidisciplinary skills across engineering domains, hardware, software, and sophisticated AI, including adaptive control systems, vision, and perception systems – all of which make them more capital-intensive than we would like.

This category of new systems has begun and will continue to change as many underlying building blocks, components, and models mature, and AI makes it easier to develop software. Many of these advancements come from the autonomous vehicle space, and Founders with this experience will be exceptionally well-positioned to apply their learnings to other domains where the systems packaging approach is the best way to capture value and meet customers’ needs. Some companies currently building AI Infused complex systems in the extended Flybridge portfolio include AeroVect, Alloy Enterprises, Agtonomy, BotBuilt, Bowery, Clockwork, DexAI, Glimpse, HaloBraid, Integral, and Intramotev.

5. AI native offerings

What are the out-of-the-box ideas for new products and services that don’t yet exist? In some ways, this question is the hardest one to answer — and yet represents exciting opportunities. Each new discontinuous platform shift enables creative Founders to build vertically integrated startups that have the potential to create entirely new industries. For example, Uber’s end-user value proposition could never be contemplated until virtually every potential customer had a GPS-enabled computer in their pocket or bag.

While enabling AI technology is advancing rapidly, translating this innovation into consumer value relies on human strengths – creativity, empathy, and intuition for user needs. Founders operating at this intersection of cutting-edge AI and human-centric design will thrive and create new categories and unforeseen applications we can not live without ten years from now. This intersection between advanced AI and insightful human design will lead Founders to redefine product utility, shifting existing paradigms to embrace new, more intuitive experiences. Some current companies in the Flybridge portfolio building to this future vision include BoldVoice, Decipad, Oasis, and Splice.

The step-change we have all witnessed in AI’s capabilities — from improving decision-making to achieving a level of cognition and task completion that rivals human benchmarks — is just the beginning. We are excited about the potential opportunities across all five dimensions in the coming decade. If you are a Founder building to this AI-powered future, don’t hesitate to reach out. We invest exclusively in AI startups from pre-seed to seed, typically leading rounds. You can learn more about Flybridge on our website.

I’ve been obsessed with AI and its impact on our world for decades. This obsession led to several investments in the field, as I described four years ago in my blog posts on Applied AI: Beyond the Algorithm and The AI Paradox. So like many others, I have watched the evolution of generative AI and ChatGPT with keen interest.

At our Flybridge investment team meeting earlier this week, my colleagues asked how the explosion in the AI market compares to previous tech trends I have seen emerge over the last nearly 25+ years. Spoiler alert: I’ve been a VC for a looong time – see my reflections on 25+ years here).

While the move to the cloud (looking at you, MongoDB), mobility, and the rise of consumer social apps were all significant developments over the previous 15-20 years, they pale in comparison to the sudden change in the market over the last 12 months brought about, primarily by OpenAI and the launch of first GPT-3, more recently ChatGPT, and the rapid advances from other players such as Google.

In particular, I am struck by the speed of adoption and the incredible ubiquity and breadth of impact that the Large Language Models ( LLMs) and Generative AI already have. Today Groupthink is our always-on collaborative AI research assistant (picture a stateful marriage between ChatGPT, Google Search, and your favorite collaborative apps, and that’s Groupthink); we use the AI-powered no-code tool Blaze to build internal apps, Aiera provides me real-time transcriptions and AI-generated summaries of Wall Street events, Brighthire streamlines our hiring insights and processes with AI-powered interview summaries and transcripts, Proscia’s AI pathology platform will analyze my skin biopsy from the dermatologist, and my college-age son can use Teal to customize cover letters based on his resume and a potential job’s needs. And that is just an illustrative sample from our small Flybridge portfolio. Everything Everywhere All at Once, indeed.

(It should be noted that Everything Everywhere All at Once was an incredible movie and my clear Best Picture Winner winner from 2022.)

The closest analogy is the excitement I felt when I first opened the Mosaic browser to explore the worldwide web in early 1994. At the time, there was a rush to define companies as “web or dot com” companies, but that quickly became a meaningless distinction as every company leveraged the global connectivity and accessibility the web uniquely enabled to solve problems and create new markets. The same will hold for today’s new “dot AI” companies, as very quickly, there will be no such thing as an AI company, as the underlying technology will be leveraged across every new and existing application to drive unique value for customers and end-users. As with the first web applications, there will be value in being a first mover, but the real value will come from harnessing the underlying technical enablers in unique and new ways to solve real problems. For B2B founders, this will typically mean starting with a vertical focus, incorporating the AI into existing business processes and workflows, and in a way that is not AI for AI’s sake but rather with a laser focus on driving business value.

There is a lot of hand-wringing about whether this technical step function will change the nature of the economy, and perhaps not for the better. Similar concerns were raised with the rise of the internet in the mid to late 90s, but instead, it unleashed a creative explosion of new ideas, tools, and solutions. As my favorite movie of 2022 shows, there is an incredible opportunity to harness humankind’s unique creativity to build magical experiences and creative solutions to real-world problems. We could not be more excited to back this generation of founders harnessing the power of AI to build everything.

When a friend of Flybridge’s first introduced us to Roy Akerman and Ori Amiga, the co-founders of Rezonate, we were immediately excited and impressed by their insights, leadership, deep technical expertise, and ability to recruit talent. Roy was previously the head of the Israeli Cyberdefense Operations, and Ori led R&D for this unit, and both received the Medal of Honor for their contributions to Israel’s National Security. After serving their country, they both had successful careers in start-up cybersecurity companies, including Cybereason, where Roy launched several new products.

We also loved the problem they were targeting: protecting the most critical cloud systems by eliminating attackers’ opportunity to breach cloud identities and access. Securing identities and, therefore, access, for both humans and machines is the key to protecting the cloud. Yet, cloud infrastructure’s growth, complexity, and ever-changing nature make this a difficult problem to crack. Rezonate’s disruptively simple approach is to, in real-time, discover, analyze, profile, and protect every identity, user, and resource across all cloud assets, preventing and stopping attacks quickly. We introduced the company to several potential customers in our diligence and received nothing but positive feedback on their approach. The cloud security market is large and growing fast, reflecting the importance of protecting cloud assets. Analysts estimate total spending of $33B today and project a growth rate of over 18% per year to $106B in 2029.

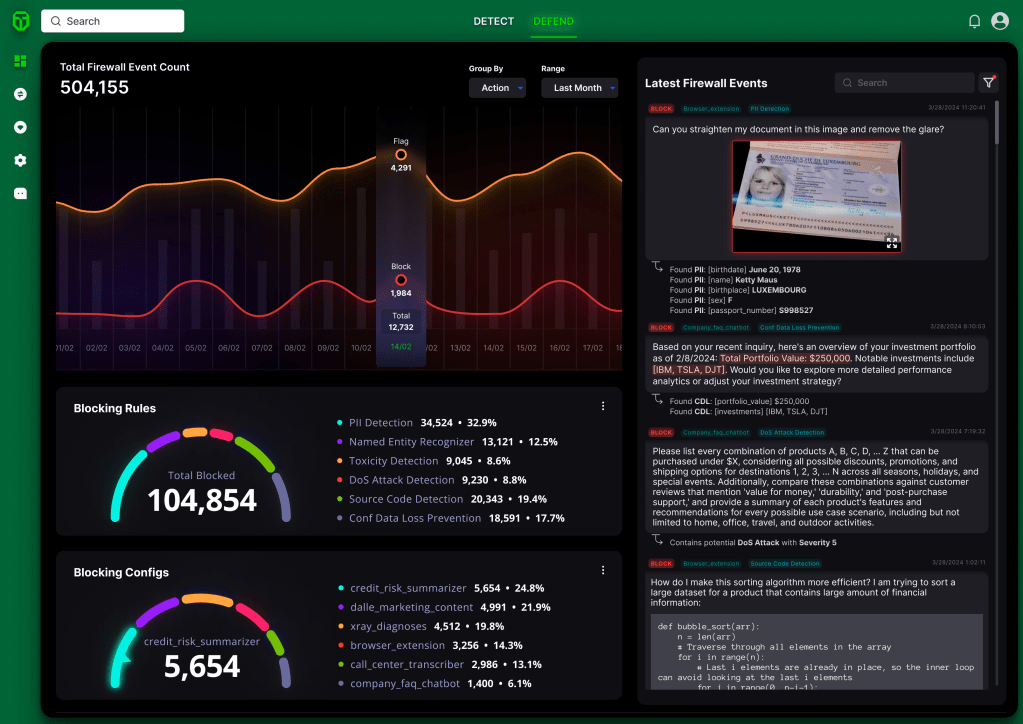

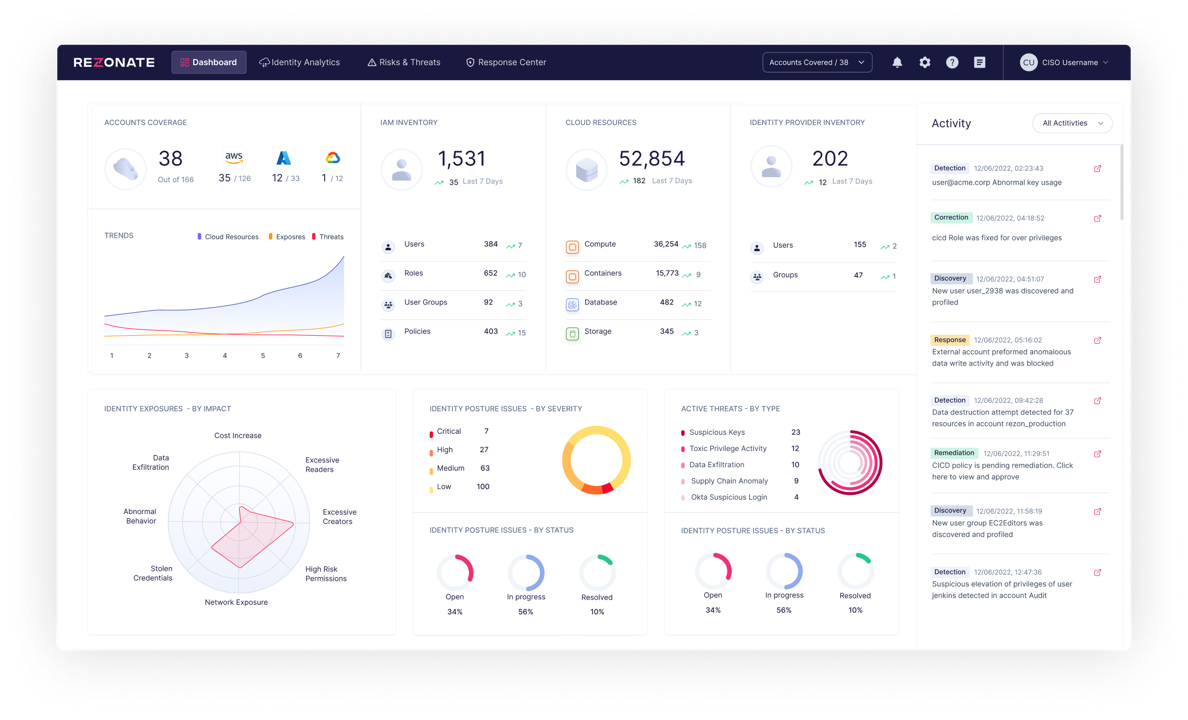

With strong founders with unique product insights into a significant, critical, and timely market opportunity, we were thrilled to co-lead the company’s seed round alongside State of Mind Ventures, toDay Ventures a Merlin Ventures seed fund, and several prominent angel investors. Since our investment, the company has made great strides and executed exceptionally well — building an exceptional team, developing the product (screenshot below), landing several design partners, and converting them into paying production customers.

Rezonate recently came out of stealth mode, and has been featured in TechCrunch, VentureBeat, and Forbes. We are confident in the future of this talented team and their innovative solution to cloud security!

Conventional wisdom for founders of early-stage venture-backed companies is that it is best practice to send out monthly investor updates – and we agree. We see a significant correlation between success and the companies whose founders maintain the discipline to follow this best practice. Much has been written about what format to use and why this is important for investors (here are a couple of links for reference here and here), but very little is written about why it is important for founders and their teams in the first place.

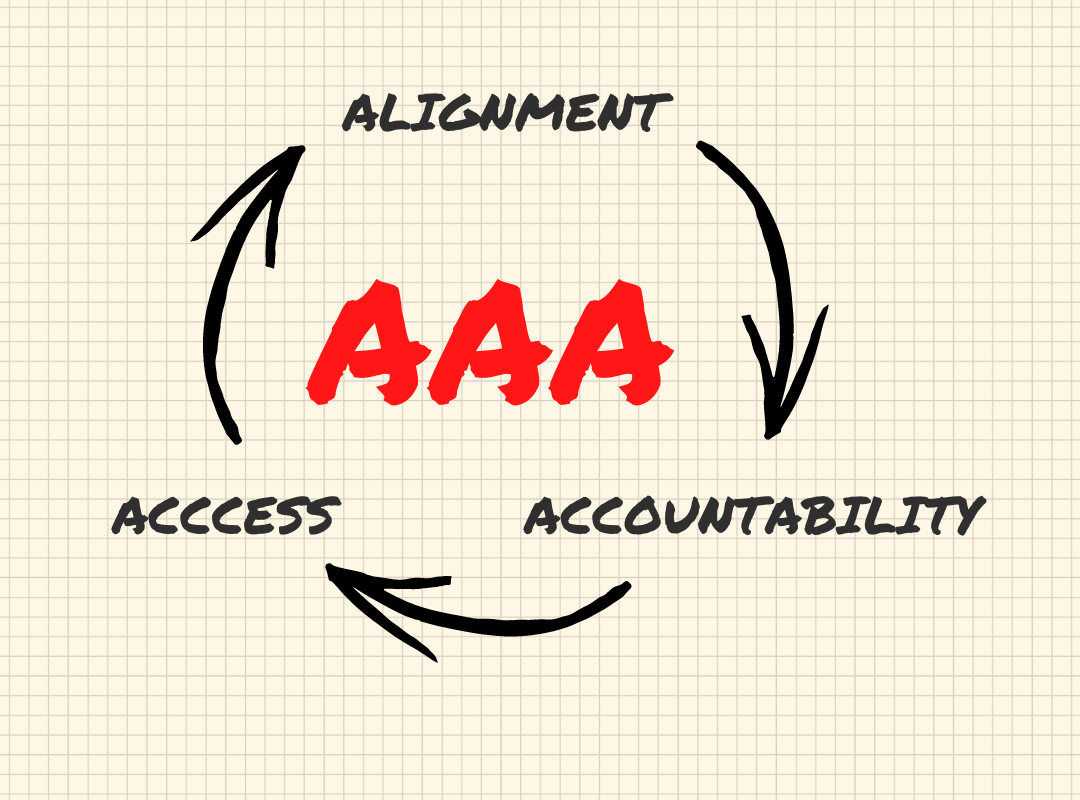

This distinction is important because while it might be easy to fall out of the habit of doing something for someone else, it’s much easier to maintain a habit when it is for you and the objective of having your company and team to be as successful as possible. Centering the monthly update and tying it to your bottom line is a game-changer. To keep it simple, keep in mind the Triple-A rubric:

Alignment: the pace of a start-up can be frenetic, with constant on-the-fly decisions. Taking a moment each month to pause, and reflect on the company’s goals, accomplishments, strategy, tactics, and needs is important for you as the founder to make sure you are focusing on the most important issues and for your team to share and understand that same focus. As one of our founders, who has written a monthly update every month since early 2020 from pre-launch and $0 in ARR to over $8M in ARR, says “while the subject line says Investor Update, I am really writing for me. It allows me to pause the first Sunday over every month and reflect on the business – what we have done well, what needs improvement, where there are gaps in my team, and what I need to make sure I personally focus on in the coming month”. This founder uses the same content for their All hands to make sure the team is equally focused and aligned.

Accountability: as a leader, you know the importance of accountability in terms of driving results, focus, and creating a high-performing team and while this most often comes from within, using external accountability to build internal accountability can be a powerful force for action and results. As one of our founders said, “I don’t think founders should rely on others to hold themselves accountable. But it still feels bad to write the same thing twice in an e-mail. The practice of sitting down to send an update builds in internal accountability.”

We firmly believe that start-ups win because they execute more rapidly and effectively than larger organizations, and if knowing that you are reporting on results to a broader audience than just yourself on the margin increases the likelihood that a key product feature is shipped on time, or sales to close as forecasted, is only goodness. If your team also knows that you are reporting more broadly, it increases the likelihood that they too will share the same degree of urgency. Finally, the monthly part of the month update, versus quarterly, reinforces this focus on speed of execution.

Access: as a small team, the extended network of advisors and investors can be invaluable in generating sales leads, potential partnership opportunities, candidates to join your team, how to compensate them, and insights into the key issues you are wrestling with at any point in time. When you formed your cap table you likely thought deeply about why each investor was involved in the company, and the monthly update can be one important way to realize that potential. As another founder noted, “As a founder, I’m confident that I have the most context to make decisions. But realistically I will never see as many startups as an investor has, and investor pattern matching is an important input to take into account. If an investor has seen 90% of successful startups do X in a similar situation, the founder should have a solid reason to not do X.” Further, there is significant research on people and companies that seem to regularly “get lucky”, but in reality, that luck is a result of building relationships, showing gratitude, and being open to new ideas and connections, all of which is facilitated by the monthly update.

The most common failure pattern we have observed over the years is not not starting to send our monthly updates but rather stopping when things are uncertain or going less well than expected. This is understandable – no one likes to share bad news and to be transparent with issues and uncertainty, but this is exactly when your investors and advisors can be most supportive as they have likely encountered similar situations in the past or may be able to open doors, make connections, ask questions that can be helpful in navigating through the uncertainty or just provide emotional support. Two anecdotes in this regard, one positive, one negative:

We were pre-seed investors in one company that found its initial product-market fit was just not there. They shut down this focus, iterated, explored, went through a “summer of despair”, and eventually landed on what seemed like a promising new focus. Never once did they fail to send out a monthly update. When the new direction started bearing early signs of fruit just as cash was running low, we were thrilled to invest more in the company to give the time and resources needed to get to milestones that allowed them to raise a large seed round from a new investor. Why? We obviously believed in the new direction, but equally importantly we had been part of the entire journey and saw just how effectively the team was able to execute during difficult times.

We were small pre-seed investors in a company where the founder “went dark” and stopped sending updates until finally reaching out to let us know that the assets of the business had been sold to another company for essentially nothing even though based on the last update things seemed to be going well (financing fell through). As it turns out, the CEO of the acquirer was a close (non-obvious) friend of ours, and yet because we never knew of the challenges, we were not able to have any impact on the result. Could this relationship have been leveraged into “getting lucky” with the acquisition at a higher value, we will never know but think that perhaps yes. In other words, you never know what and who your extended family of supporters knows unless you ask.

A last and final incentive, if the above was not enough. Sending monthly updates is time-efficient. When you stop sending updates, it increases the likelihood of multiple inbound calls and, especially if you have a large-cap table, you will spend far more time doing one-off calls than the time it takes to share the same information with everyone consistently.

In terms of the format and approach to monthly updates, we will not rehash the existing materials out there, but encourage you to:

Keep the format simple and consistent. It is much easier to send every month if you are not starting from scratch.

Block out time and stack it with other administrative tasks so you both get it done and don’t interfere with important sales or product work.

Share issues and things that have not gone well. This increases trust and increases the likelihood of generative conversations with your investors and advisors.

Always make asks/have a “how you can help” section. If you are heads down executing, it is ok for this to be “no asks this month”.

Thank people who have helped in the prior month. This increases the likelihood that others will help in the future.

At the bottom, rehash the company’s mission and what you do as noted in the linked examples above.

So send your monthly investor updates. Not for us, but for you and your success.

Leading-edge software developers are amazing – yet incredibly demanding – early adopters. For products and platforms that increase development velocity, remove complexity, and drive performance and scalability, their initial support is a leading indicator of future success. Companies that channel this early support into creating a passionate, engaged, developer community build better products, see stronger adoption, and ultimately build better businesses than their non-community-driven peers. This is an important investment theme for Flybridge and one we have seen play out successfully with our prior investments in companies such as MongoDB, which is now a $30+B value public company whose industry-leading database has been downloaded over 200 million times from their website, and Firebase, which now has more than 3 million apps using its services and in which we were seed and Series A investors prior to their acquisition by Google in 2014.

Fast forward to 2021 and one of the fastest-growing developer communities is forming around Appwrite. Initially developed by Founder and CEO, Eldad Fux, as a passion project to solve his own problems (as all the best developer platforms are), the Appwrite community has exploded in the last 9 months growing to over 50K members and over 375 code contributors across the globe. Developers love the platform, which now has over 13,000 Github stars, making it one of the fastest-growing repos on Github, and usage is up 24 times in the last 6 months. The passion for and engagement with Appwrite can be seen in their most recent release, where open source contributors outnumbered maintainers and over 100 community-driven pull requests were merged into the main branch.

Appwrite is a secure open-source backend server for web, mobile & flutter developers, that is often referred to as an open-source version of Firebase. Google has been an excellent steward of Firebase, but nearly 10 years after its initial release which enabled real-time applications, and after integrating several acquisitions, we and the Appwrite community believe there is an opportunity to create the leading backend service for the next 10 years.

Specifically, Appwrite was written from the ground up to be the best backend as a service on the market, with consistently designed services that drive a better developer experience and APIs that are designed to work well as a whole, yet with the flexibility to be consumed separately. All the protocols are ones that developers already know, which shortens the learning curve and the time to wow. Finally, in today’s multi-cloud, privacy-aware, and security-focused world, Appwrite can be hosted on any infrastructure, location, and platform which allows application developers to control their data, users’ privacy, and comply with local regulations.

Given this success, we were thrilled to co-lead the company’s recently announced $10M Seed round alongside Bessemer, Ibex Investors, and Seedcamp. The resources will be used to expand the team (careers page here) and drive the roadmap, including releasing Appwrite 1.0 and the Appwrite Cloud service as well as deepening the platform’s database, storage, authentication, and functions services, all while being responsive to new ideas brought forward from this incredible community. We look forward to the journey!

Venture capital partnerships such as ours are small and hire new partners infrequently. As a tight-knit, cohesive partnership that very much works together as a team, getting this right is especially important. A year ago, as we were early in investing out of our 2019 fund and looked forward to launching a new Flybridge fund 12-24 months from now, we decided to add a new General Partner to our team. We knew it would be the most important decision we would make this year.

We cast a wide net, hired a recruiter, reviewed 100s of candidates, and met with dozens. Our criteria were simple: we were looking for someone that was wildly curious, with tremendous investment judgment, who approached venture investing with innate founder empathy, brought with them a deep appreciation for the power of community and the connections to back that up. Importantly, we wanted someone who would fit seamlessly into our team – valuing our long history of working together while challenging us to lead in new directions.

With today’s announcement that Anna Palmer is joining the Flybridge team as a General Partner, we (immodestly) crushed this decision. Jeff, Jesse, and I are beyond thrilled to welcome Anna to the Flybridge Family.

I first met Anna in late 2012 when she launched her first company, FashionProject, out of the TechStars community. Immediately struck by her raw intelligence, creativity, and passion for making a difference through entrepreneurship, we stayed in touch as she built FashionProject into the industry leader in online designer clothing donation, building a community of tens of thousands of members and non-profits across 36 countries. But it was not until after the election in 2016 that we began to work together as collaborators and partners.

Anna identified a significant unmet investment opportunity in companies founded by women and wanted to partner with the Flybridge team to form a venture fund focused on investing in female-founded companies pursuing billion-dollar opportunities. Aligned with her vision and inspired by her ability to galvanize change, we jumped at the chance and formed XFactor Ventures.

Anna created XFactor’s unique model: we are a team of women, other than me, that are all current founders of venture-backed companies that are investing at the earliest of stages behind the next generation of founders seeking to build transformative companies. As active founders ourselves, we know first-hand the ups and downs of building a company and seek to support our portfolio founders with capital and the connections and mentorship to navigate the company building journey. We launched XFactor in July of 2017 and have since grown our community into an investment team of 22 founders in 6 cities and nearly 60 portfolio companies across two funds with over 80 amazing women founders and co-founders.

As we worked together over the last four years, in addition to seeing her drive in creating and building XFactor, we saw her instincts as an investor as she personally led seven investments for XFactor — including in Chief, Zubale, and MixLab — that are all performing incredibly well. Anna is extremely curious, can see connections from one industry that apply to another, has an excellent feel for important trends in the marketplace, and a natural sense for what companies will drive outsized value in the future. Not to mention she did all of this part-time while also launching, with a co-founder and our investment capital, her second company, Dough, from our offices.

Fast forward to September of this year. Driven by Anna and the investment team’s talents, the breadth of their networks, and the depths of their insights, XFactor’s success proved yet again that in early-stage venture investing, relationships and expertise are all that matter. XFactor’s network and expertise are very complementary to ours and there was clearly an opportunity to align our investment efforts more closely while still preserving the power of XFactor’s unique model. Thus, we leaped at the chance to add Anna to our team when she decided to become a full-time investor after Dough had reached a level of maturity such that she could hand over the CEO reins to her talented co-founder, Vanessa Bruce. Starting work 24 hours after saying yes, Anna joined to help us kick off our annual Founder’s Week, and in partnering together full-time over the last two months, it is like we have been working together for years…which, of course, we have been.

Anna will focus on the full range of B2C and B2B opportunities with a specific interest in community-driven companies, commerce 3.0 (logistics, discovery, payments, social commerce, small business solutions), marketplaces, and the everyday economy while also continuing to drive XFactor Ventures forward. You can read more on her Medium post here and follow her on Twitter here, but on behalf of the entire Flybridge community, please join me in congratulating Anna and welcoming her into our team!

4 Success Factors for Early-Stage Venture Investors

This article is the final installment and a summary of a six-part series that was posted on the Flybridge Medium page outlining my experience on what it takes to be a great venture investor.

Whether you’re new to venture capital or simply honing your craft, these four ideas will help you stay grounded as you evaluate, commit to, and nurture investments in your portfolio.

Massive winners define great venture capitalists and great venture capital funds. The best investors fully internalize this power-law of venture returns and seek to back companies that can become “outliers”. Massive wins are all that matters in driving outcomes.

A key to investing behind the best companies is to identify macro market trends early and to ride the waves of growth they create. High growth companies need the wind at their back, so investing early behind emerging trends that develop quickly creates an environment for young, growing, businesses to flourish.

To be a great investor, you need to master the cycle of Seeing-Selecting-Winning-Investing-Supporting-Harvesting. “SSWISHing means you need to see many opportunities, select the best ones, win your way into hot deals, support your companies’ growth, and navigate a path to generating liquidity from your investments. Each stage feeds off the others.

The best-expected-value returns are most likely the companies in your portfolio that are killing it, so lean into your winners with more capital. Smart follow-on decisions should be married with a starting portfolio of more, rather than fewer companies, to account for the inevitable randomness in returns and performance.

I would like to thank my Flybridge partners Jeff Bussgang and Keegan Forte; all my XFactor partners, but especially Danielle Morrill, Aihui Ong, and Anna Palmer; the Columbia Business School students in Angela Lee’s class, “Foundations of VC”, that saw an early presentation on this topic; and my family for their collective input to and inspiration for these posts, although as always any mistakes and omissions are all mine.

4 Success Factors for Early-Stage Venture Investors

4 Success Factors for Early-Stage Venture Investors